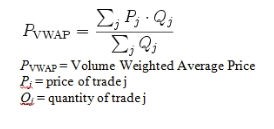

VWAP (Volume Weighted Average Price) is the ratio of the total price of an instrument weighted by its traded volume divided by the total volume over a given period of time. ProphetX implements the time as the user supplied number of positions specified by the Period parameter.

Parameters

Period Number of positions specifying the domain over which to calculate the volume weighted average price for a given position. For a given position (p) and Period (n) the price-volume domain is given by the range of values [from p through p-n-1] inclusive.

Formula

for j = 1,n where n is the Period. This is calculated for every position in the VWAP array.