Implied volatility is one of the deciding factors in the pricing of options. Options, which give the buyer an opportunity to buy or sell an asset at a specific price during a pre-determined period of time, have higher premiums with high levels of implied volatility, and vice versa. Implied volatility approximates the future value of an option, and the option’s current value takes this into consideration.

It is important to remember that implied volatility is based on probability. It is only an estimate of future prices rather than an indication of them.

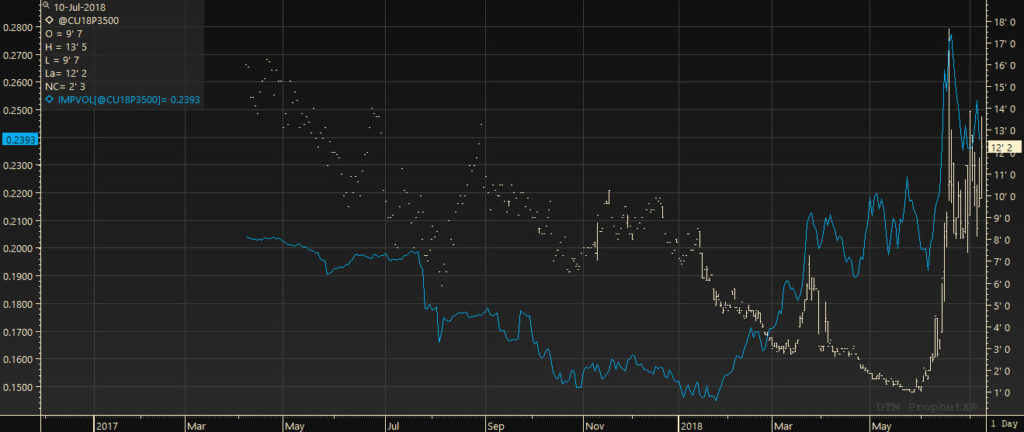

Example of a chart with the Implied Volatility study